Most banking contact center agents still search through PDFs, outdated intranets, and SharePoint wikis to answer basic customer questions.

That leads to long call times, inconsistent answers across channels, and compliance risks when agents share outdated information.

Customer experience in banking is usually an operational problem. The quality of every interaction depends on whether the agent or self-service system can find the right answer fast from an approved knowledge base.

This article breaks down what customer experience management in banking looks like. You’ll learn the challenges banks face and strategies to improve CX across your contact center.

What Is Customer Experience Management in Banking?

Customer experience management (CEM) in banking is the process by which a bank designs, delivers, and improves every interaction a customer has with the institution. That includes phone calls, branch visits, mobile app usage, online banking, email, chat, and self-service portals.

CEM is about making sure that every channel delivers accurate, consistent, and timely service. Behind every touchpoint is either a person or a system that must provide the right information.

This matters more now than it did five years ago for a few reasons:

- Banking products are largely the same. Most banks offer similar savings accounts, credit cards, and loan products. When the products look alike, CX becomes the deciding factor. Forrester’s CX Index found that customer-obsessed organizations report 41% faster revenue growth and 51% better customer retention than those that aren’t.

- Fintech and Neobank competitors have raised the bar. Customers who use digital-only banks expect frictionless service. They compare their banking experience to those apps, not to other traditional banks.

- Every customer interaction in banking carries regulatory weight. An agent sharing outdated compliance information isn’t just a bad experience but a potential audit finding.

Challenges of Managing Customer Experience in Banking

Improving CX in banking isn’t as simple as upgrading an app or adding a chatbot. The industry has structural problems that make CX harder to fix than in most other sectors.

Unregulated Knowledge Behind Regulated Conversations

Banking agents provide information that can trigger regulatory consequences. Incorrect answers to loan eligibility questions or outdated fee guidance can lead to compliance violations and audit findings.

But the systems agents rely on to find those answers aren’t held to the same standard. Most banks store policies across shared drives, PDFs, wikis, and email threads. None of these has version control, approval workflows, or automatic expiry.

Front-End Investment, Back-End Neglect

Banks have spent heavily on mobile apps, online portals, and digital onboarding. Customers see polished interfaces. But agents often work with outdated intranets, old search tools, and knowledge bases that haven’t changed in years.

The front end gets the budget because it’s visible to customers. The back end doesn’t because it’s visible only to agents. But agents are the ones answering calls, handling disputes, and explaining policies. When their tools are slow or disorganized, it doesn’t matter how good the app looks.

Product Complexity Without Centralized Knowledge

A retail bank might offer savings accounts, term deposits, credit cards, personal loans, home loans, business lending, insurance, foreign exchange, and superannuation. Each has its own policies, eligibility rules, fee structures, and regulatory requirements.

No amount of onboarding can prepare an agent to memorize that volume of detail, especially when products change regularly. It’s a knowledge access problem.

When that knowledge is spread across multiple systems with no central structure, agents either spend too long searching or give answers based on what they remember. What they remember may not be current.

Institutional Knowledge Lost to Turnover

When an experienced agent leaves, they take practical knowledge that no system can replicate. Which loan exceptions apply to long-standing customers? How to handle a dispute that falls outside the standard workflow. Which compliance step do new hires miss most often?

A new agent starts from scratch, follows standard procedures, gives an incomplete answer, and the customer escalates.

Expectations Set by Faster-Moving Industries

Customers don’t compare their bank to other banks. They compare it to every digital service they use. And most of those services are faster and simpler than anything banking offers today.

Banks operate under constraints most industries don’t: regulatory requirements, complex products, and multi-jurisdiction compliance. But customers don’t factor that in. They just want the same speed and clarity they get everywhere else.

These problems compound across thousands of calls, chats, and branch visits every day. The strategies that follow address each of them.

10 Strategies to Improve Customer Experience in Banking

Each strategy below targets a specific CX problem in banking contact centers, with practical steps you can start applying to your operations:

Centralize Knowledge So Agents Deliver Consistent Answers

When knowledge lives in multiple places, no one controls which version is current. A policy gets updated in one system but not in another. One agent finds the new version and quotes the correct fee. Another finds the old one and quotes something different. The customer gets two answers to the same question, and trust drops.

The fix is pulling all policies, product information, and procedures into a single searchable knowledge base. Instead of storing content as long documents, structure it as direct answers that agents can scan and relay quickly. Tag each article by product, process, and channel so the right answer surfaces in seconds regardless of who’s searching.

For example, if a customer asks about early mortgage repayment penalties, every agent should pull from the same source and give the same answer, whether they’re on the phone, in chat, or at a branch.

Build Omnichannel Consistency Across Every Touchpoint

Offering phone, chat, email, app, and branch support doesn’t make a bank omnichannel. Multichannel means customers can reach you through different channels. Omnichannel means every channel gives the same answer because they all pull from the same source.

Most banks don’t have this. The website FAQ sits with marketing. The chatbot content belongs to the digital team. The contact center knowledge base is owned by operations. Each team updates on its own schedule, which means a policy can change on Monday and still show the old version in the chatbot two weeks later. Customers notice when the website says one thing and the agent says another.

Connecting all customer-facing channels to a single governed knowledge source solves this. When a policy changes, it updates once and pushes everywhere. The agent on the phone, the chatbot, and the website all display the same information at the same time, because the content only exists in one place.

Reduce Average Handle Time Without Sacrificing Quality

Long calls cost money and frustrate customers. But telling agents to “keep calls short” doesn’t work if they’re still searching through PDFs and policy documents mid-call.

The fix here is to remove search time. Replace unstructured documents with a searchable knowledge base that returns direct answers. For multi-step processes like dispute resolution or loan modifications, use decision trees that guide agents through each step rather than requiring them to interpret a 40-page policy.

Operationalize Compliance in Every Customer Interaction

Most banks treat compliance and customer experience as separate workstreams. Compliance teams update policies in their own systems. CX teams manage what agents see. The gap between the two is where risk lives, because a regulatory change can take days or weeks to reach the contact center floor.

Building compliance into the knowledge system closes that gap. Every article gets an owner, a review date, and an approval workflow. When a regulation changes, the system flags affected content, routes it through compliance review, and pushes the updated version to agents. The old version archives automatically with a full audit trail.

Role-based access controls add another layer. Junior agents see only approved frontline content. Sensitive risk procedures stay restricted to authorized staff.

This means agents always work from the most current, approved content, which is how compliance rates improve without relying on manual email chains or last-minute briefings.

Cut Onboarding Time for New Agents

Banking contact centers have high turnover. And every new agent needs to learn a complex product portfolio: savings, loans, cards, insurance, deposits, and foreign exchange. Traditional training tries to get agents to memorize this. It takes weeks, and much of it is forgotten within days.

Instead of training agents to memorize, give them a system that makes memorization unnecessary. A structured knowledge base with guided decision trees lets new hires serve customers from their first week. They search for the answer, follow the guided workflow, and deliver the same outcome as a 5-year veteran.

For example, a customer calls to ask whether they can split their home loan into fixed and variable portions. With a structured knowledge base, a new agent can search “home loan split,” find the article, and walk the customer through eligibility criteria and next steps in under four minutes.

Personalize Service Interactions Beyond Marketing

Banks have become better at personalizing product recommendations. You get a credit card offer based on your spending patterns or a savings prompt based on your balance. But when you call with a problem, the agent treats you the same as every other caller.

Service personalization means the agent sees your context alongside the answer. This can include:

- Your account tier

- Your recent interactions

- Your product portfolio

- Your history with the bank

To make this work, the knowledge system needs to connect with your CRM and core banking platform.

For example, if a high-value customer calls about a credit card charge, the agent sees that this person has been with the bank for 12 years, holds three products, and had a similar issue resolved last month. They can acknowledge that context and offer a tailored resolution instead of reading a generic script.

Deploy Self-Service That Draws From the Same Knowledge Base

Self-service only works when it gives the same answers agents do. If your chatbot says one thing and your agent says another, self-service creates problems instead of solving them.

Most banks build self-service on a separate content layer. The website FAQ is maintained by one team, the chatbot by another, and the contact center knowledge base by a third. They drift apart over time.

Fix this by connecting self-service channels to the same governed knowledge base your agents use. When a policy changes, it updates everywhere at once. The customer who checks international transfer fees on the website and the agent who answers the same question over the phone both work from the same source.

This does two things. First, call volume drops because customers can actually resolve questions on their own. Second, when they do call, the agent confirms what they already saw online instead of contradicting it.

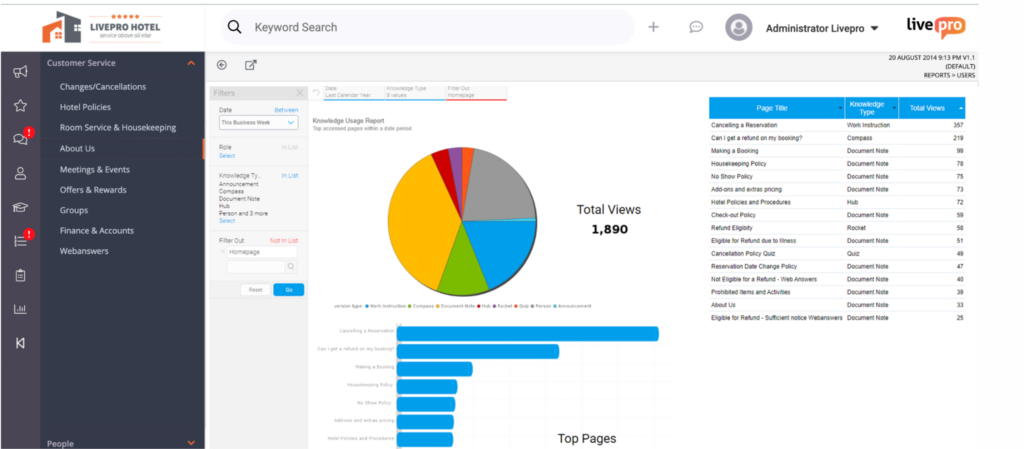

Use Knowledge Analytics to Find CX Gaps

Most banks measure CX through surveys. NPS, CSAT, CES. These tell you how customers feel after the fact. They don’t tell you what went wrong during the interaction or why.

Knowledge analytics fills that gap. They track what customers ask about, where agent searches fail, which articles get negative feedback from agents, and which content hasn’t been updated in months. These signals surface problems in real time before they appear in survey scores.

For example, if analytics show that “fee waiver policy” searches spike every Monday after weekend charges post, content managers can simplify that article before it drives more calls and complaints. If a specific product article has a high abandonment rate, it probably needs restructuring.

Automate Routine Inquiries With AI-Powered Voice and Chat

Deploy an AI in your contact center that draws from the same governed knowledge base your agents use. The AI handles routine calls automatically and escalates complex ones to human agents with full context.

This matters for two reasons:

- FCall volume on routine queries drops, freeing agents to spend time on complex, high-value interactions such as disputes, loan inquiries, and complaint resolution.

- Customers get faster service for simple questions because they don’t have to wait in a queue behind someone with a complex problem.

Engage Customers Proactively Before Problems Escalate

Most banking support is reactive. The customer has a problem, calls the bank, and waits. By that point, they’re already frustrated.

Proactive engagement means reaching out before the problem turns into a complaint. To make this work in practice:

- Set triggers based on transaction data. Balance approaching overdraft? Send an alert with options. Deposit maturing? Notify the customer a week early.

- Use knowledge analytics to spot emerging patterns. If searches for a specific issue spike, reach out to affected customers before they call.

- Make every proactive message actionable. An alert without a next step is noise.

- Track impact on reactive volume. If overdraft alerts reduce overdraft-related calls by 20%, that’s a quantifiable return.

When done right, reactive call volume drops and retention improves. Preventing a bad experience is always more efficient than fixing one later.

How livepro Helps Banks Deliver Better Customer Experience at Scale

livepro is an AI-powered knowledge management platform built for contact centers. It gives banking teams a single platform to create, govern, and deliver knowledge across every channel, with AI-powered search, guided workflows, compliance controls, and real-time analytics.

Instead of agents searching through PDFs, wikis, and shared drives mid-call, livepro delivers direct answers from one governed source. Content stays current through automated review cycles and approval workflows. And every answer agents access is verified, version-controlled, and audit-ready.

Here’s how livepro helps banking contact centers reduce handle time, stay compliant, and improve customer experience:

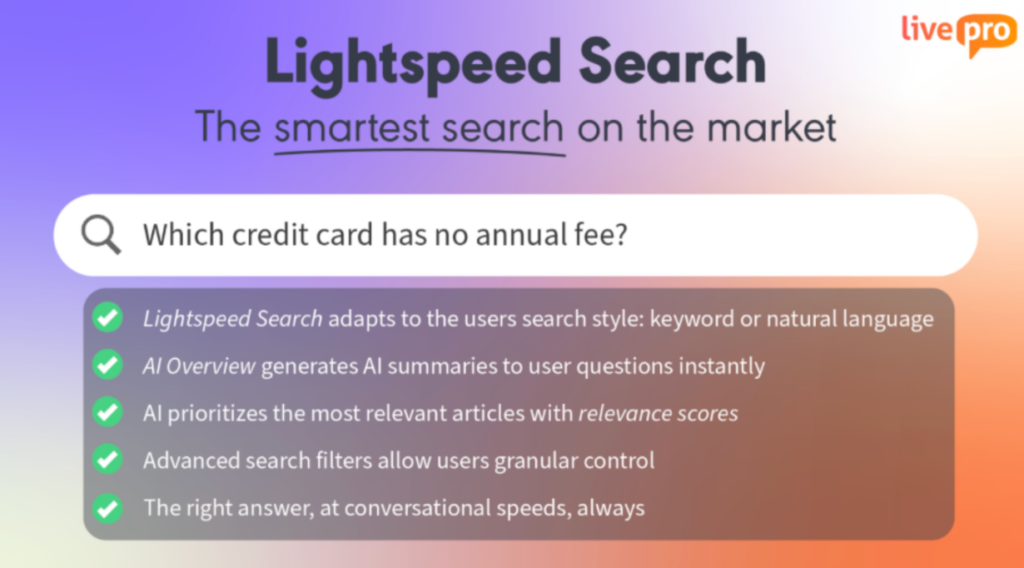

Hybrid Lightspeed Search for Faster Answers

livepro’s Hybrid Lightspeed Search focuses on what the agent is trying to accomplish, not just the keywords they typed. It accounts for role, context, and query intent to surface the most relevant answer first. Results are ranked by likelihood of being correct, with the best match at the top.

For example, an agent types “customer disputing a charge from two months ago.” Instead of returning every article that mentions “dispute,” livepro surfaces the specific time-bound dispute process, the eligibility window, and the resolution steps in a single ranked result.

Automated PII Detection for Data Protection

Knowledge authors in banking regularly document real scenarios to make content practical: how a specific dispute was handled, what a KYC exception looked like, how a fraud case was escalated.

In the process, real customer data like account numbers, card details, or tax file numbers can end up inside published articles. Manual reviews don’t catch these consistently, and a single exposure can trigger violations across multiple frameworks.

livepro continuously scans knowledge content using AI-driven pattern recognition to catch PII before it reaches agents:

- Uses regex and machine learning to detect formats like credit card numbers, SSNs, IBANs, and account identifiers

- Redacts detected PII automatically or flags it for admin review based on your configuration

- Supports real-time scanning during authoring and scheduled batch scans across the full knowledge base

For example, an author documents a fraud escalation process and includes a real customer’s card number as a reference. livepro detects the card format during authoring and replaces it with a redacted placeholder before the article is saved. The process documentation stays intact. The customer data never reaches the published version.

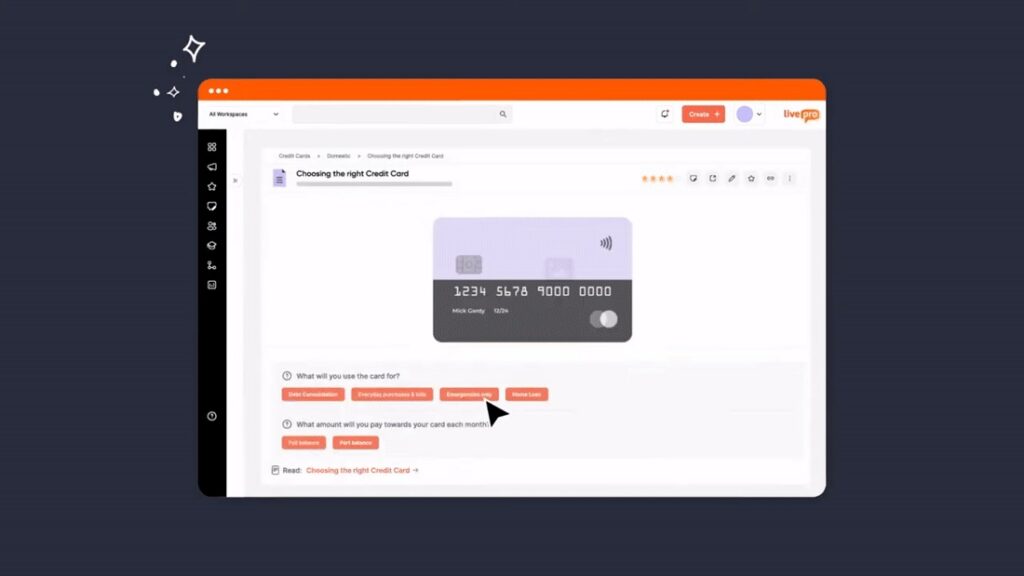

Decision Trees for Consistent, Error-Free Processes

Banking processes have multiple decision points that depend on variables like transaction type, customer segment, account status, and regulatory jurisdiction.

When agents work through these by reading policy documents, each agent interprets the logic differently. One agent approves a fee waiver that another agent would deny. Customer satisfaction depends on who picks up the phone.

livepro’s Decision Trees (called Rockets) remove that inconsistency by converting complex procedures into guided workflows with branching logic:

- Agents answer simple questions at each step (yes/no, select from options, enter a value)

- The system determines the next step based on the answer and guides the agent forward

- Every path leads to an approved outcome with the correct next action and customer communication.

Knowledge Governance for Compliance-Ready CX

Banking policies change often. Fee structures update quarterly. Regulatory thresholds shift with new rulings. Product terms change with market conditions.

Without a system that keeps pace, outdated content stays live and agents reference it on calls without knowing it’s wrong.

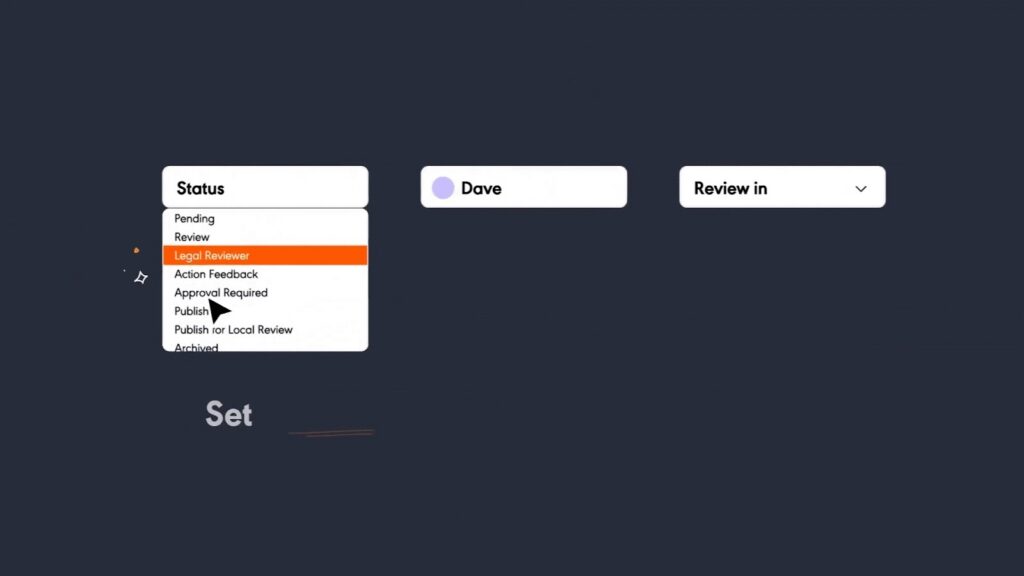

livepro embeds governance into every stage of the content lifecycle:

- Version History: Every edit creates a new version with the author, timestamp, and change notes so teams have a complete record.

- Automated Review Schedules: Articles trigger review notifications based on set dates or expiry rules. Overdue content gets flagged before agents see it.

- Approval Workflows: Content follows a defined path from draft to review to approval to publish. Nothing goes live without sign-off.

- Announcements: When a policy updates, livepro sends real-time alerts inside the platform so agents know immediately and follow the latest version.

- Archiving: Outdated versions move out of circulation but stay searchable for audit reference.

For example, a bank updates its credit card fee disclosure to reflect new regulatory requirements. The content owner submits the revision, the compliance reviewer approves it, and the updated article is published automatically. The previous version archives with a full change log. When auditors ask what was live on a specific date, the answer is available in seconds.

Knowledge Analytics for CX Visibility

livepro’s analytics dashboards shows how knowledge is being used across the contact center in real time:

- Article Performance: Which policies or procedures do agents access most, and how long they spend on each. Articles with high access but long read times likely need simplification.

- Search Behavior: Which searches succeed, fail, or get abandoned. Failed searches point directly to missing content that needs to be created.

- User Engagement: Usage trends by branch, team, or individual agent. Low engagement in a specific team may signal a training need or a content gap.

- Content Currency: Articles that haven’t been reviewed or updated recently. Compliance-critical content like KYC checks or dispute procedures can’t afford to go stale.

For example, analytics show that “card chargeback process” searches spike every Friday afternoon, but the article has a 60% abandonment rate. The content team rewrites it for clarity, adds a decision tree for the most common chargeback scenarios, and tracks whether search success improves the following week.

Luna AI Voice Agent for Routine Banking Inquiries

Luna is an AI voice agent built to handle customer calls without human involvement. It listens to the caller’s question in real time, parses the intent using natural language processing, and responds with the correct answer from the bank’s verified knowledge base.

Here’s how it works:

- The customer speaks or describes their query

- Luna’s NLP engine identifies the intent

- Luna pulls the approved answer from the centralized knowledge base

- If the query is complex, Luna escalates to a human agent with full context of the conversation

Every interaction is transcribed and analyzed for quality and compliance, giving CX leaders visibility into what customers ask about outside business hours and where automated responses need improvement.

Self-Service (Web-Answers) for Channel Consistency

When customers find one answer on the website and hear a different one from an agent, trust breaks. This happens when self-service channels pull from a separate content source that updates on a different schedule than the contact center knowledge base.

livepro’s Web-Answers connects customer-facing channels directly to the same governed knowledge base agents use.

When content updates, it reflects across every channel simultaneously. Customers and agents always work from the same information.

Case Study: How ME Bank Improved CX With Knowledge Management

ME Bank is one of Australia’s leading direct banks, with over 400,000 customers and no physical branches. The contact center is the primary point of contact for every customer interaction.

The Problem

Agents relied on an internal wiki built in SharePoint to find answers during calls. The wiki was hard to organize, difficult to search, and required extensive training just to navigate. Average handle time sat at 10 minutes per call. Staff satisfaction was declining.

The Solution

ME Bank replaced its wiki with livepro. Agents gained access to structured, searchable answers via an intuitive interface rather than dense wiki pages. The system required far less training and let agents find the right answer in seconds.

The Results

- 40% reduction in AHT, from 10 minutes to 6 minutes per call

- 92% of staff found the new system useful

- 61% more staff said information was accurate and up-to-date

- 39% more staff said information was easy to find

- 38% more staff reported having access to all the information they needed

Shorter calls, more confident agents, and accurate answers added up to a better experience for ME Bank’s customers on every interaction.

Book a demo to see how livepro helps banking contact centers cut handle time, close compliance gaps, and give agents the answers they need in seconds.

FAQs

Why is knowledge management important for banking CX?

Banking CX depends on whether agents can deliver accurate, compliant answers during live customer interactions. Knowledge management gives them a single, governed source to find answers in seconds, rather than searching across disconnected systems. When agents find answers faster, handle time drops, accuracy improves, and customers get a consistent experience across every channel.

What role does AI play in banking customer experience?

AI helps banking contact centers work faster without sacrificing accuracy. AI-powered search understands what an agent is trying to accomplish and surfaces the most relevant answer, not just keyword matches. AI voice agents handle routine inquiries like balance checks and payment confirmations automatically, freeing human agents for complex issues like disputes and loan inquiries.

How do you measure customer experience in banking?

Most banks track NPS, CSAT, and customer effort scores. But these are lagging indicators. They tell you how customers felt after the fact.

Operational metrics give you a clearer, real-time picture: average handle time, first-call resolution rate, compliance rate, agent onboarding time, and knowledge search success rate. The strongest CX measurement programs connect both. When AHT drops, and FCR rises, CSAT and NPS tend to follow.

What is the difference between customer service and customer experience in banking?

Customer service is one part of customer experience. It covers the interactions where a customer reaches out for help: a call, a chat, or a branch visit. Customer experience is broader. It includes every touchpoint a customer has with the bank: the app, the website, the onboarding process, the statements, the marketing, and yes, customer service. A bank can have good customer service but poor customer experience if the rest of the journey is frustrating.

What are some key trends in customer experience management in banking in 2026?

The biggest shifts in 2026 are around AI-powered service delivery, proactive engagement, and operational CX measurement. Banks are moving from reactive support to proactive outreach based on transaction data.

AI voice agents and chatbots are handling a growing share of routine inquiries. And CX teams are shifting from survey-based measurement to real-time analytics that track knowledge usage, search success, and content gaps. The common thread is that CX is becoming an operations function, not just a design or marketing one.